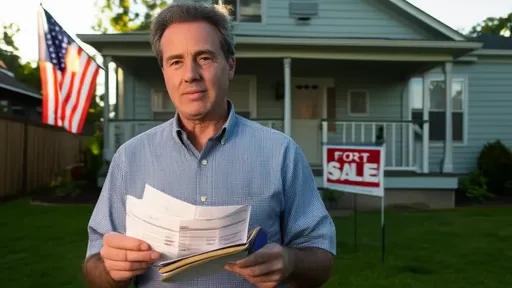

Why Your Luxury Watch Investment Could Backfire Without This Move

So you’ve bought a rare Rolex, thinking it’s a smart play for long-term gains. But what if I told you that one overlooked detail—tax compliance—could wipe out your profits? I’ve seen collectors get blindsided by unexpected liabilities. This isn’t just about passion; it’s about playing it smart. Let’s break down how staying compliant isn’t just legal sense—it’s financial strategy. The truth is, luxury watches have evolved from personal indulgences into serious alternative assets. Over the past decade, certain models have outperformed traditional investments, with some vintage pieces appreciating over 300%. But behind the gleam of polished steel and intricate dials lies a complex web of financial responsibilities. Many collectors focus solely on acquisition and resale value, ignoring the regulatory framework that governs these transactions. When tax obligations are overlooked, what starts as a rewarding hobby can quickly turn into a costly lesson. This article will guide you through the often-missed intersection of horology and tax law, showing how proactive compliance doesn’t just protect—it enhances the value of your collection.

The Hidden Risk in Luxury Watch Collecting

Luxury watch collecting has transformed significantly over the years. Once considered a niche pastime for enthusiasts, it is now a recognized segment of the alternative investment market. High-end timepieces from brands like Rolex, Patek Philippe, and Audemars Piguet regularly fetch six- and seven-figure sums at auction, drawing interest from both seasoned collectors and institutional investors. However, this growing financialization brings with it a set of responsibilities that many overlook. Unlike publicly traded stocks or bonds, luxury watches are tangible assets that do not generate automatic tax reporting. There is no 1099 form issued when you sell a rare Daytona at auction, nor does your bank flag a private sale between collectors. This lack of institutional oversight creates a false sense of invisibility—many assume that if no one is watching, no rules apply. But tax authorities in major economies are increasingly aware of the high-value secondary market for watches and are tightening enforcement.

One of the most common misconceptions is that personal use items are always tax-exempt. While many countries allow limited exemptions for the sale of personal belongings, these exceptions are narrow and often do not apply to high-value collectibles. For example, in the United States, the IRS does not distinguish between a hobbyist and an investor based on intent alone. If you sell a watch for significantly more than you paid, the transaction may be classified as a taxable event regardless of whether you consider yourself a casual collector. The same principle applies in the UK, Canada, Australia, and most European nations, where capital gains tax can be triggered by any disposal of an asset that has appreciated in value. The risk is amplified when collectors engage in frequent buying and selling, which can signal a pattern of trading behavior—something tax authorities interpret as a commercial activity.

Consider the case of a collector in Germany who purchased a vintage Omega Speedmaster in 2010 for €12,000 and sold it in 2022 for €68,000. Because the holding period was less than ten years, the gain was subject to income tax under German tax law. Without proper documentation or reporting, this transaction could result in penalties, interest, and even a full audit of past acquisitions. Similarly, in France, any sale of a collectible valued above €5,000 must be declared, and failure to do so can lead to fines of up to 80% of the undeclared gain. These are not theoretical risks—they are real enforcement actions taken by tax agencies that now use data analytics and international cooperation to track high-value private sales. The lesson is clear: passion does not exempt you from fiscal responsibility.

When Buying Becomes Taxable: Understanding the Triggers

It’s a common assumption that tax obligations only arise when money changes hands—specifically, when a profit is made. While that’s partially true, the reality is more nuanced. Taxable events related to luxury watches are not limited to sales. They can also be triggered by importation, gifting, inheritance, and even relocation. Each of these actions exists within a legal gray area for many collectors, who often treat their watches like personal belongings rather than financial assets. But tax systems are designed to capture value transfers, not just cash transactions. Understanding what constitutes a taxable moment is the first step in avoiding unintended consequences.

Take cross-border movement, for example. If you purchase a rare Patek Philippe in Switzerland and bring it into the United States for personal use, you may still owe customs duties and import taxes. The U.S. Customs and Border Protection agency assesses duties based on the declared value of imported goods, and luxury watches often fall into higher tariff categories. Even if you’re not selling the watch, bringing it into the country for long-term use can be interpreted as an importation event. Some collectors attempt to avoid this by declaring items as “used personal effects,” but this only works if the watch was genuinely owned and used abroad prior to relocation. Authorities are increasingly scrutinizing such claims, especially when multiple high-value items are involved.

Selling is, of course, the most direct trigger. But even here, the rules vary. In the United Kingdom, the Capital Gains Tax (CGT) system includes a “chattels exemption” for personal possessions sold for less than £6,000. However, this exemption does not apply if the total proceeds from all collectibles sold in a tax year exceed £15,000. Moreover, if a watch is considered “wasting property”—defined as having a useful life of less than 50 years—it may be exempt. But most luxury watches, especially mechanical ones, are built to last far longer, disqualifying them from this category. In Canada, the situation is similar: while personal-use property is generally not taxed on gains, listed personal property—including rare watches—must be reported when sold, and any profit is taxable.

Private sales are another area of risk. Many collectors prefer to sell directly to other enthusiasts through forums or social media, believing these transactions are invisible to authorities. But tax agencies are adapting. Platforms like eBay and PayPal now report certain transactions to tax authorities under information-sharing agreements. While smaller peer-to-peer sales may not be automatically flagged, large transfers of funds can raise red flags. In one documented case, a collector in Australia was audited after receiving a $90,000 bank transfer from an overseas buyer. Without a proper invoice or explanation, the transaction was treated as unreported income. The takeaway is simple: no transaction is truly off the radar. Awareness of triggers allows collectors to plan ahead, report accurately, and avoid penalties.

Capital Gains and Collectibles: A Different Tax Animal

One of the most critical distinctions in tax planning is understanding how luxury watches are classified. In most jurisdictions, they do not fall under the same category as stocks or real estate. Instead, they are treated as collectibles—a unique asset class with its own set of rules. This classification has direct implications for tax rates and liability. In the United States, for example, the long-term capital gains rate for most investments is capped at 20%. However, for collectibles, including rare watches, the rate is 28%, regardless of the taxpayer’s income bracket. This 8-percentage-point difference can significantly erode net returns, especially on high-value transactions.

The rationale behind this higher rate is rooted in policy. Governments view collectibles as non-productive assets—they do not generate income, create jobs, or contribute to economic output in the same way as businesses or real estate. As a result, they are often taxed more heavily to discourage speculative behavior and ensure fairness in the tax system. While this may seem unfair to serious collectors, it reflects a broader regulatory philosophy. The 28% rate applies not only to watches but also to art, antiques, coins, and precious metals. What’s more, short-term gains—on watches held for less than one year—are taxed at ordinary income rates, which can exceed 37% for high earners. This means that flipping a rare watch quickly for profit could result in more than half the gain going to taxes.

Jurisdictional differences further complicate the picture. In France, collectibles are subject to a flat tax rate of 30% on capital gains, combining both income tax and social charges. In Italy, the “salva-risparmi” decree provides some relief, but only if the asset has been held for at least five years. Japan applies a progressive tax system to capital gains, with rates ranging from 15% to 55%, depending on income. Meanwhile, in Singapore and the United Arab Emirates, there is no capital gains tax at all, making these locations attractive for high-net-worth collectors. However, residency matters—moving a collection to a tax-free jurisdiction does not automatically erase liability if the owner remains a tax resident elsewhere.

Holding period is another key factor. Many countries offer reduced rates or exemptions for long-term ownership. In Germany, for instance, capital gains on private assets are tax-free if the item is held for more than ten years. This creates a powerful incentive for collectors to adopt a long-term strategy. A watch purchased for €20,000 and sold after eight years for €100,000 would be fully taxable. But if the same watch is held for twelve years, the gain disappears from the tax ledger. This kind of planning is not about evasion—it’s about aligning collecting behavior with legal frameworks to maximize after-tax returns.

Documentation: Building Your Audit-Proof Paper Trail

If there’s one practice that separates savvy collectors from those who get into trouble, it’s documentation. In the world of luxury watches, provenance is everything—not just for authenticity, but for financial and legal protection. Tax authorities do not accept memory or verbal claims. They require evidence: receipts, invoices, service records, and ownership history. Without these, a collector may be unable to prove cost basis, leading to higher taxable gains or even penalties for underreporting.

The foundation of any audit-proof collection is the purchase record. Whether buying from an authorized dealer, a gray market vendor, or a private seller, always obtain a detailed invoice. This should include the date of purchase, model and serial number, condition, price paid, and seller information. For high-value transactions, consider using escrow services that provide additional verification. Many collectors also keep digital scans of original packaging, warranty cards, and authentication letters from manufacturers. These documents not only support value claims but also demonstrate good faith in maintaining the asset’s integrity.

Service records are equally important. Every time a watch is serviced—especially by an authorized center—request a detailed report. These records show ongoing investment in preservation and can help establish a timeline of ownership. They also serve as indirect proof of value, as high-end servicing can cost thousands of dollars. Shipping logs, insurance appraisals, and photos taken over time further strengthen the paper trail. Some collectors maintain a digital ledger, updating it with each transaction or significant event. Cloud storage with backup ensures these records survive even if physical documents are lost.

When it comes to resale, documentation directly impacts net proceeds. A buyer is more likely to pay a premium for a watch with full paperwork, and a seller with complete records can confidently report gains with accurate cost basis. In contrast, a “naked” watch—sold without papers—may fetch less and raise suspicion during tax review. In one case, a collector in the UK was unable to prove he had paid £18,000 for a Rolex Submariner and was forced to accept a default cost basis of zero, resulting in tax on the full sale price. Proper documentation isn’t just about compliance—it’s about preserving value at every stage of ownership.

Cross-Border Moves: The Silent Tax Trap

Traveling with a luxury watch collection can be a minefield of unintended tax consequences. Whether you’re taking a single timepiece on vacation or relocating your entire portfolio to a new country, the rules governing personal imports vary widely. What seems like a harmless act—wearing a watch across the border—can trigger customs inspections, duty assessments, or even confiscation if not handled correctly. The core issue is the distinction between personal use and commercial import. Most countries allow travelers to bring in personal items duty-free, but only if they are genuinely for private use and not intended for resale.

Problems arise when collectors own multiple high-value watches or frequently rotate pieces between residences. Authorities may interpret this as evidence of commercial activity, especially if the individual has a history of selling watches or operates a blog or social media presence around collecting. In the European Union, for example, bringing a watch into a member state from outside the bloc may require declaration if its value exceeds €430. While this threshold is low, enforcement is often lax for single items. However, if a traveler carries three or more luxury watches, customs officials may assume they are part of a commercial shipment, leading to full valuation and taxation.

Relocation poses an even greater risk. When moving to a new country, expatriates often bring their personal belongings, including watches, under temporary import or personal effects exemptions. But these exemptions come with conditions. In Japan, for instance, imported personal effects must have been owned and used for at least six months prior to the move. In Switzerland, collectors must declare all items and may be required to post a bond, which is refunded only if the items are re-exported. Failure to comply can result in retroactive duties and penalties.

The solution lies in proactive planning. Before any international move, consult the customs regulations of the destination country. Keep detailed records of ownership and usage, including photos of you wearing the watches in your home country. For high-value collections, consider obtaining a Carnet de Passages—a customs document used for temporary importation of valuable goods. Widely accepted in over 80 countries, it allows collectors to bring watches across borders without paying duties, provided they are re-exported within a set period. This tool is commonly used by art collectors and classic car owners and is equally valuable for horology enthusiasts. By treating cross-border movement with the same seriousness as a financial transaction, collectors can enjoy global mobility without tax surprises.

Working with Experts: When to Call a Pro

No one expects a watch collector to be a tax expert. The systems are complex, constantly changing, and vary by country. Yet knowing when to seek professional help can mean the difference between smooth sailing and a costly audit. The key is recognizing red flags—situations that signal increased risk and warrant specialized advice. These include high-value sales, international relocation, inheritance planning, and frequent trading activity.

When selecting an advisor, look for professionals with experience in both tax law and alternative assets. A general accountant may not be familiar with the nuances of collectibles taxation. Instead, seek out firms that specialize in high-net-worth individuals or have a dedicated art and collectibles practice. Credentials matter—check for certifications such as CPA (Certified Public Accountant), EA (Enrolled Agent), or membership in professional organizations like STEP (Society of Trust and Estate Practitioners). Avoid self-proclaimed “luxury tax gurus” who promise guaranteed savings or offshore solutions with little transparency.

Ask the right questions. A competent advisor should be able to explain how your country treats collectibles, what records are necessary, and how to structure sales for optimal tax outcomes. They should also be familiar with international reporting requirements, such as the U.S. FBAR (Foreign Bank Account Report) or the Common Reporting Standard (CRS) used by over 100 countries. A good consultant doesn’t just solve problems—they help you build a sustainable, compliant strategy.

Consider the value of preventive advice. Paying a few thousand dollars for a tax review before a major sale or move can save tens of thousands in liabilities. Some collectors schedule annual check-ins with their advisors, treating compliance as part of their collection management routine. This proactive approach not only reduces risk but also provides peace of mind, allowing them to focus on what they love—appreciating the craftsmanship and history behind each timepiece.

Smart Compliance as a Competitive Edge

Compliance is often seen as a burden—a necessary evil to avoid trouble. But for the modern collector, it can be a strategic advantage. A well-documented, tax-compliant collection is more liquid, more trusted, and more valuable in the marketplace. Buyers prefer watches with clean ownership histories, knowing they won’t inherit tax complications. Auction houses and dealers are more likely to accept consignments from sellers who can prove provenance and cost basis. Even insurers offer better terms when records are complete.

Moreover, compliance enhances credibility. In a market where authenticity is constantly challenged, a collector who maintains rigorous standards stands out. This reputation can open doors to exclusive sales, private networks, and invitation-only events. It also strengthens negotiating power—when a buyer knows the paperwork is in order, they are more likely to close the deal quickly and at a fair price.

Finally, compliance supports long-term wealth preservation. By aligning collecting habits with tax rules, enthusiasts can maximize after-tax returns, avoid penalties, and pass assets smoothly to heirs. A collection that grows in value and remains legally sound becomes a true legacy—not just of taste and passion, but of financial wisdom. In this light, tax planning isn’t a distraction from the joy of collecting. It’s an essential part of it. The most successful collectors don’t just chase rarity and performance—they build systems that protect and amplify their gains. In doing so, they turn regulatory diligence into a quiet but powerful edge.